The increasing connectivity of the global economy, along with the Federal Reserve’s monetary policy decisions, often triggers significant market reactions. Historically, major Fed rate cuts have had a profound impact on global financial markets, resulting in a spectrum of immediate and extended effects.

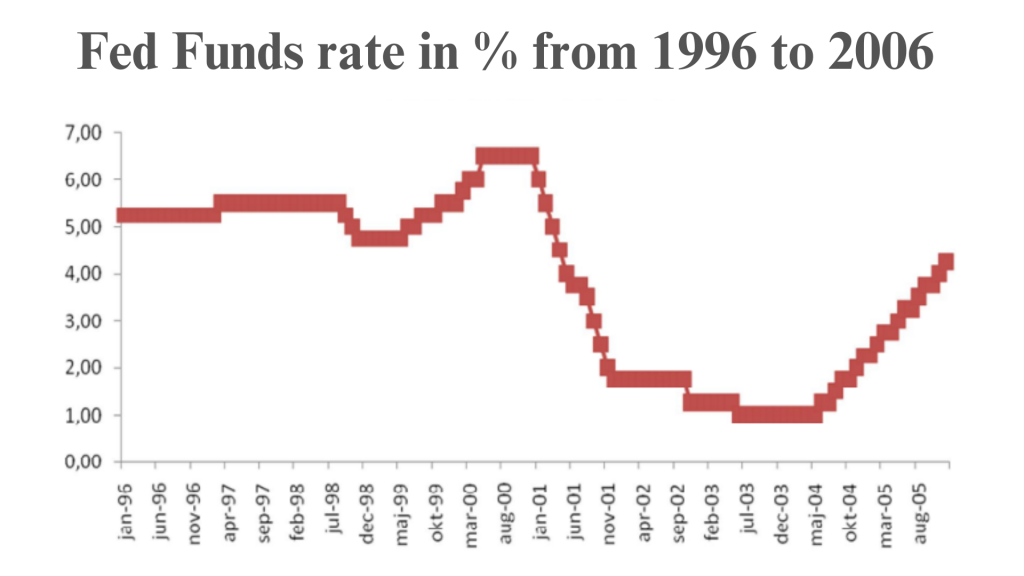

After the dot-com bubble burst in the early 2000s, the Federal Reserve responded by sharply lowering interest rates, from 6.00% at the start of 2001 to 1.75% by the end of that year. These rate cuts were intended to ease the economic slowdown and boost investor confidence. The dot-com bubble, driven by excessive speculation in tech stocks, saw the NASDAQ index climb over 300% between 1998 and 2000, only to fall by 75% by 2002. Key moments like Netscape Communications Inc.‘s August 9, 1995 IPO and Alan Greenspan’s 1996 warning on “irrational exuberance” drew attention to the overheated market.

The Fed’s policies significantly influenced the bubble’s growth and its aftermath. From 1995 to 1999, the Fed kept rates low, encouraging risky investments. Even though there was a brief rate hike in 1997, it was quickly reversed, continuing the trend of easy money. In 1999, the Fed began raising rates to cool down the overheated market, but when the economy slowed in 2001, rates were slashed again, from 6% to 1.75% in just one year. These rapid shifts in monetary policy, combined with global reactions to changes in liquidity and investment trends, created a lot of volatility in markets. Although the rate cuts temporarily supported economic growth, they had long-term effects, contributing to global market instability and later financial crises.

1998 Fed Rate Cuts: Global Currency Crisis

In 1998, the Federal Reserve made a series of rate cuts to address the international economic turmoil that had begun to impact the U.S. economy.

On September 29, 1998, the Fed reduced the Federal Funds Rate by 25 basis points to 5.25%. This was followed by another 25 basis points cut on October 15, bringing the rate down to 5.00%.

The interest rate cut sent stock prices soaring around the world. According to the New York Times, the Dow Jones industrial average gained 330.58, its third-biggest point gain ever, to close at 8,299.36, its highest level since August 26. Bond prices also surged. The dollar, which had been sliding sharply against the Japanese yen, fell again. Finally, on November 17, the Fed made a further 25 basis points reduction, setting the Federal Funds Rate at 4.75%.

These cuts were triggered by a sequence of global financial crises. The Asian financial crisis, which began in Thailand in 1997, spread through Asia and Latin America, culminating in a severe currency crisis in Russia in late 1998.

Those global events destabilized financial markets and pushed Long-Term Capital Management (LTCM), a major U.S. hedge fund, to the brink of collapse. LTCM, with $4.8 billion in equity, heavily leveraged itself by borrowing over $125 billion and engaging in derivatives contracts exceeding $1 trillion. When LTCM’s investments failed in the summer of 1998, the potential liquidation of its portfolio posed a global financial threat.

In a brief statement accompanying the September 1998 rate cut, the Fed explained that the action was intended to cushion the impact of declining foreign economic conditions and tighter domestic financial conditions on the U.S. economy.

2001 Fed Rate Cuts: The Dot-Com Bust and 9/11

Following the burst of the dot-com bubble and the onset of the 2001 recession, the Fed implemented a series of rate cuts. Starting with a 50 basis point reduction in January 2001, the Federal Funds Rate was cut progressively through the year. By December 2001, the rate had been lowered from 6.00% to 1.75%, with both 50 and 25 basis point cuts applied at various points to stimulate economic growth and address the downturn.

The dot-com bust led to a significant stock market decline, with the Nasdaq Composite Index peaking in February 2000 and not bottoming out until September 2002. The ensuing economic downturn led to a contraction in GDP, higher unemployment, and an eight-month-long recession.

The 9/11 terrorist attacks intensified these economic challenges. The Fed’s aggressive rate-cutting strategy aimed to reduce these adverse effects, with a total reduction of 5.25 percentage points throughout 2001.

Fed Rate Cuts 2002–2003: Flagging Recovery, Low Inflation

After the dot-com recession, the Federal Reserve took several steps to support the struggling economy and address low inflation. “With inflationary expectations subdued, the committee judged that a slightly more expansive monetary policy would add further support for an economy which it expects to improve over time,” the Fed said in a statement.

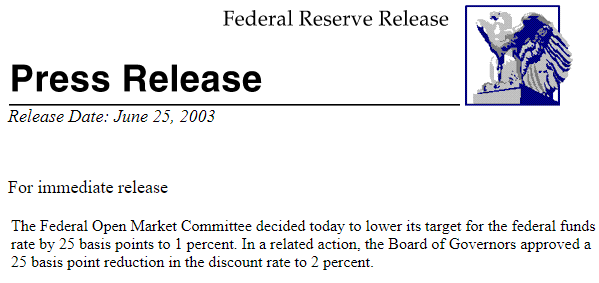

On January 3, 2002, the Fed cut the Federal Funds Rate by 50 basis points to 1.75%. As the recovery remained sluggish, the Fed made another 50 basis point cut on November 6, 2002, lowering the rate to 1.00%. Then, on June 25, 2003, the Fed reduced the rate by 25 basis points, keeping it at 1.00%, the lowest level in 45 years.

The recovery from the dot-com recession was slow, and consumer confidence remained low. The Fed’s November 2002 rate cut aimed to address “greater uncertainty” and “geopolitical risks.” By mid-2003, core PCE inflation had dropped to 1.47%, prompting another rate cut to combat deflationary pressures. The Fed’s actions resulted in the lowest federal funds rate in 45 years.

Fed Rate Cuts 2007–2008: The Housing Market Crash

As the housing bubble burst and unemployment increased in 2007, the Federal Reserve responded with a series of interest rate cuts to stabilize the economy. The Fed reduced the Federal Funds Rate from 4.75% in September 2007 to 2.00% by April 2008, including notable reductions of 75 basis points in January and March 2008.

After concluding its rate-hiking campaign in June 2006, the Fed began cutting rates as the economic downturn intensified. Within less than a year, rates were slashed by 2.75 percentage points to stimulate growth and address economic risks. By April 2008, Fed Chair Ben Bernanke paused to evaluate the impact of these cuts.

Although there were concerns about potential inflation, the full scope of the forthcoming global financial crisis was not fully anticipated. As Richard Yamarone once noted, prolonged negative real rates could trigger significant inflation pressures, an issue that would soon become evident.

Initially, the lower rates helped buoy stock markets and restore some confidence. However, persistent underlying economic issues, such as declining corporate profits and continued market uncertainty, meant that the effects of the rate cuts were temporary. While they provided short-term relief, they also contributed to excessive risk-taking in financial markets and led to a protracted recovery period.

During the financial crisis, the Fed further reduced the federal funds rate from 5.25% in September 2007 to nearly zero by December 2008. This aggressive cut aimed to stabilize financial markets and stimulate economic activity by lowering borrowing costs. However, the impact on global markets was mixed. While the rate cuts and the subsequent implementation of quantitative easing (QE) helped stabilize financial institutions and lower long-term interest rates, they also raised concerns about potential inflation and asset bubbles, contributing to market volatility and uncertainties about the long-term effectiveness of these policies.

In the mid-2000s, the Fed’s decision to hike rates was aimed at cooling off a rapidly overheating housing market. By June 2006, the Fed had increased the federal funds rate to 5.25% to address concerns about rising home prices and inflation. However, as the housing market collapsed and the financial crisis deepened, the Fed reversed course, cutting rates aggressively in late 2008.

The impact of these rate cuts was profound. On one side, they helped to stabilize the housing market and provided much-needed liquidity. On the other side, the prolonged low rates contributed to the housing market’s rebound and further fueled asset bubbles. This cycle of rising and falling asset prices demonstrated the complexity of monetary policy’s effects on global markets. While the immediate goal of stabilizing the housing market was achieved, the long-term consequences included increased market volatility and uneven economic recovery.

COVID-19-Induced Rate Cuts

The Fed’s response to the COVID-19 pandemic involved unprecedented rate cuts, dropping the federal funds rate to 0% to 0.25% in March 2020. This drastic measure was intended to support the economy during a period of severe economic disruption and high unemployment. Prior to these cuts, the Fed had already lowered rates to 1.0% to 1.25% on March 3, 2020, in response to early signs of economic strain from the pandemic.

The global spread of COVID-19 and subsequent lockdowns led to an immediate economic downturn, with April 2020 witnessing a significant loss of 20.5 million jobs and an unemployment rate soaring to 14.7%. To address the crisis, the Fed’s March 16 emergency rate cut, saying that the “coronavirus outbreak has harmed communities and disrupted economic activity in many countries, including the United States,” aimed to provide substantial liquidity through a $700 billion quantitative easing program and stabilize financial markets.

By May 2020, the economy technically began to recover after the shortest recession on record. However, the repercussions of the pandemic and the Fed’s aggressive rate cuts continue to affect economic conditions and financial stability.

Impact of COVID-19-Induced Fed Rate Cuts on the Global Financial Markets

The immediate impact of these cuts was a significant boost to financial markets. Equity indices rebounded sharply from their initial pandemic-induced lows, reflecting increased investor confidence. It was a strategic move by the Federal Reserve to cut its target federal funds rate to near-zero levels in response to the COVID-19 crisis; the aim was to lower borrowing costs and stimulate economic activity amid widespread uncertainty and disruptions.

Initially, those rate cuts effectively reduced short-term borrowing costs, providing essential liquidity to financial markets and contributing to economic stabilization. Lower interest rates, as it happens, typically led to cheaper loans, which support both consumer spending and business investment. However, the effects of these rate cuts extended beyond the U.S. market, influencing global financial currents.

A 2021 study by the National Institute of Health (NIH) researched the impact of COVID-19-induced lockdowns and interest rate cuts on global financial markets, using data from 12 countries and Special Administrative Regions (SARs) between January and July 2020. The study concluded that stock markets responded positively to both policies, with interest rate cuts having a more pronounced effect than lockdown measures. This suggests that while both policies were factored into market pricing, rate cuts had a more immediate and significant impact on market performance.

The Fed’s rate cuts prompted a search for yield, as investors sought higher returns in a low-interest-rate environment. This behavior drove increased investments in equities and higher-risk assets, contributing to heightened volatility in global stock markets. Furthermore, with reduced returns on traditional fixed-income investments, such as government bonds, investors turned to alternative assets, which amplified movements in asset prices.

The global ripple effect also impacted foreign exchange markets. The lower U.S. interest rates diminished the attractiveness of the dollar, leading to its depreciation relative to other major currencies. This depreciation influenced international trade and investment flows, making U.S. exports more competitive while increasing the cost of imports.

Moreover, the rate cuts and associated quantitative easing measures led to substantial increases in central bank balance sheets worldwide. These measures were critical for providing short-term liquidity; meanwhile, they also raised concerns about potential long-term inflationary pressures and the formation of asset bubbles. The Fed’s aggressive rate cuts were instrumental in stabilizing the U.S. economy and financial markets during the early stages of the pandemic. However, they also set off a series of global financial adjustments and uncertainties that continued to influence markets beyond 2021.

Fed’s Struggle with Post-COVID-19 Economic Challenges

In recent years, against the backdrop of an anticipated significant rate-cut decision, the Federal Reserve’s monetary policy has evolved in response to a range of economic challenges. Notably, the rate hikes implemented between 2022 and 2023 aimed to curb historically high inflation. During that period, as mentioned above, the Fed raised the federal funds rate from near zero to over 5%, which marked a sharp pivot from the ultra-loose monetary policies adopted during the pandemic era.

While these rate hikes succeeded in moderating inflation, they introduced new economic risks, including slower growth and heightened market volatility. The markets have exhibited significant instability as investors adjust to the reality of higher borrowing costs and a decelerating economy. Consequently, the Fed’s strategy for managing the post-pandemic recovery—anchored in these aggressive rate hikes—has faced scrutiny, as elevated interest rates have tightened credit conditions and contributed to economic uncertainty.

Persistent inflation remains a core challenge.

As recent indicators suggest, inflation is now driven less by rising wages and more by increases in energy, commodity, and food prices. This complex inflationary landscape is further exacerbated by factors such as ‘greenflation’—the inflationary pressures stemming from decarbonization efforts—and concentrated pricing power in key industries. In sectors plagued by supply bottlenecks, profits surged—unit profits rose by 9.4% in Q4 2022, while labor costs only increased by 4.7%; this shows a growing disparity between profit growth and labor cost increases.

The Fed’s actions have also disrupted the financial sector, as evidenced by the 2023 collapses of Silicon Valley Bank, Signature Bank, and First Republic. Within a year, U.S. banks lost over $1 trillion in deposits, leading to significant unrealized losses estimated between $1.75 and $2 trillion by mid-2023.

The convoluted effects of Fed rate cuts illuminate a fundamental truth: short-term policy changes can result in significant and enduring shifts on a global scale.

Market sentiment peaks amid uncertainty over Fed's looming rate decision - Investmentals

[…] “My guess is they’re split. There’ll be some around the table who feel as I do, that they’re a little bit late, and they’d like to get on their front foot and would prefer not to spend the fall chasing the economy. There’ll be others that, from a risk management point of view, just want to be more careful,” noted Former Dallas Fed President Robert Kaplan, pointing to the internal division within the FOMC. Kaplan’s observations indicates that the forthcoming decision could be one of the most contentious in recent history. […]